Managed Markets Headcount and Organization Study

Highlights of the report:

Download a PDF of these Highlights

Pharmaceutical manufacturers continue to evolve the staffing structures of their managed markets organizations to ensure ongoing access to their products as government policy continues to change and pricing pressures from payers heighten. HIRC's report, Managed Markets Headcount and Organization Study, assists pharmaceutical manufacturers in understanding trends in headcount across very large, large, and mid-size firms. Select key findings include:

- Headcount is up 3% year-over-year due to increases in reimbursement support, contracting administration, and clinical support.

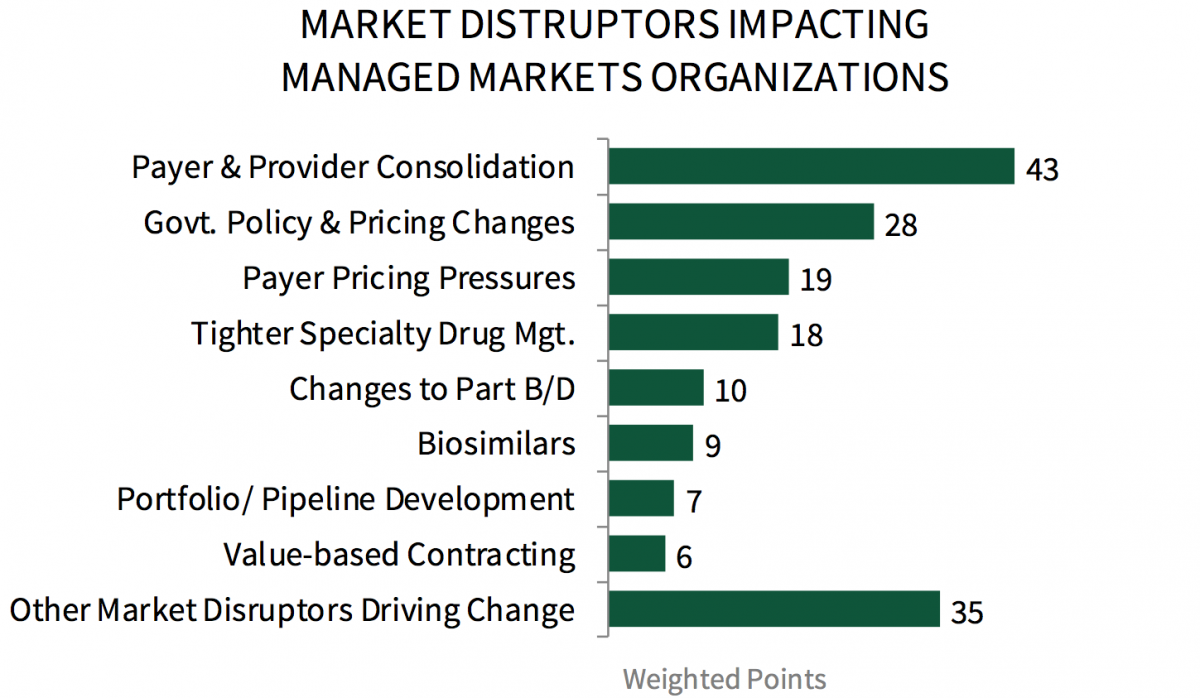

- Panelists report the biggest factors driving change in managed markets organizations for 2018/2019 were payer and provider consolidation, government policy and pricing changes, payer pricing pressures, and tighter specialty drug management.

- Account management and reimbursement support personnel comprise over half of the typical managed markets organization.

Key Finding: Pharmaceutical firms' overall managed markets headcount increased 3% year-over-year; reported changes reflect a need for greater clinical support, additional reimbursement support for patients, and effective contracting administration.

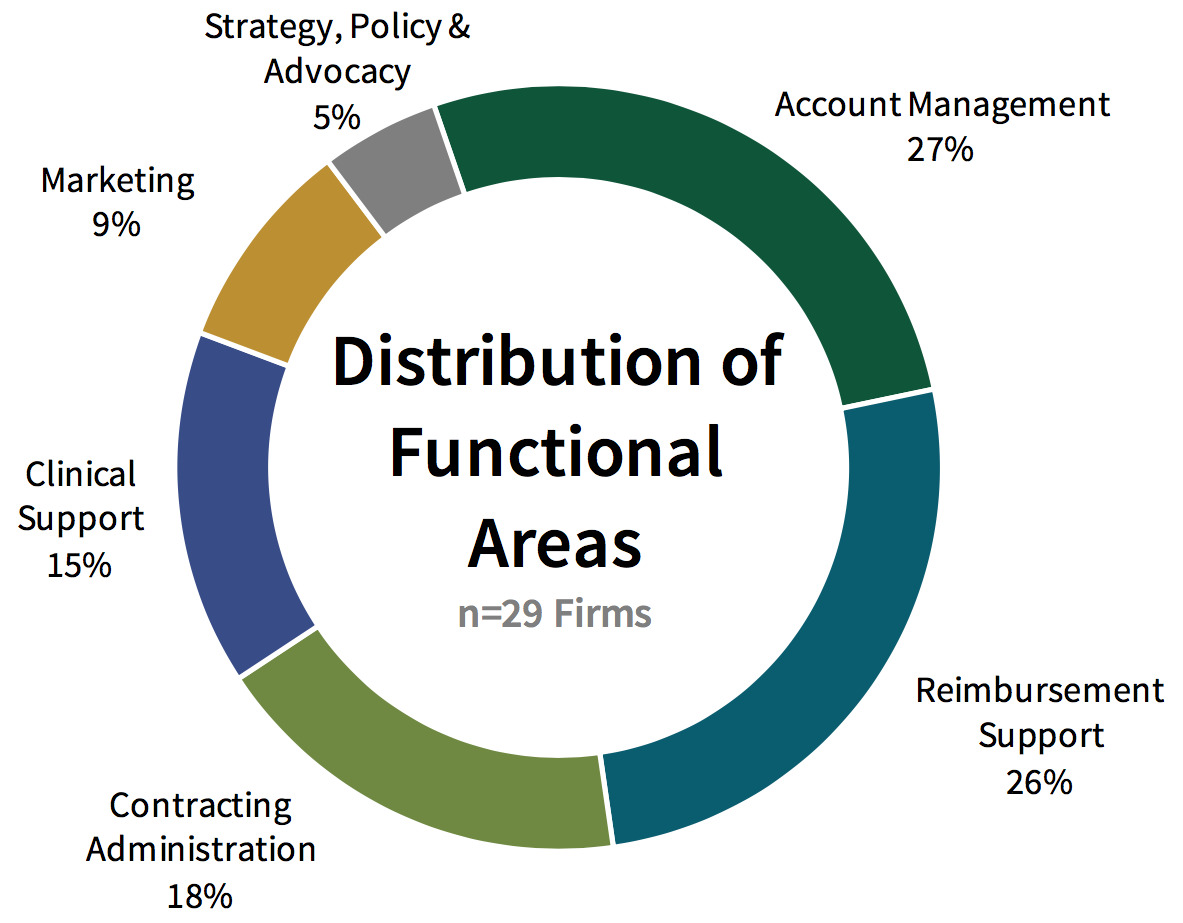

Account Management and Reimbursement Staff Comprise Over Half of the Typical Managed Markets Organization. Pharmaceutical firm's managed markets organizations are comprised mostly of account management and reimbursement support staff, with account management staff accounting for 27% of total managed markets personnel and reimbursement staff accounting for 26%.

Drivers for Organizational Changes Include Payer & Provider Consolidation, Government Policy & Pricing. Panelists were asked to list potential market disruptors to their managed markets organizational structure in 2018/2019. Respondents report payer and provider consolidation (25% of all factors) as the primary driver of potential disruption in their managed markets organizations, followed by government policy and pricing changes (16%), payer pricing pressures (11% ), and tighter specialty drug management (10%).

The full report includes detailed analyses of typical managed markets organizations of very large, large, and mid-size firms, as well distribution of and year-over year changes in managed markets headcounts across the following six functional areas:

- Account Management

- Marketing

- Reimbursement Support

- Contracting Administration

- Clinical Support

- Strategy, Policy, and Advocacy

Research Methodology and Report Availability. HIRC surveyed leading pharmaceutical companies during fall 2018 to gain insights concerning their managed markets headcount, organizational structures, and the key issues driving their staffing investments. Each company’s data are privacy-protected, and results are only reported in aggregate to ensure confidentiality. The complete report, Managed Markets Headcount and Organization Study, is available now to HIRC’s Managed Markets subscribers at www.hirc.com.

Download a PDF of these Highlights

Download Full Report (Subscribers only) >